GetApp offers objective, independent research and verified user reviews. We may earn a referral fee when you visit a vendor through our links.

Our commitment

Independent research methodology

Our researchers use a mix of verified reviews, independent research, and objective methodologies to bring you selection and ranking information you can trust. While we may earn a referral fee when you visit a provider through our links or speak to an advisor, this has no influence on our research or methodology.

Verified user reviews

GetApp maintains a proprietary database of millions of in-depth, verified user reviews across thousands of products in hundreds of software categories. Our data scientists apply advanced modeling techniques to identify key insights about products based on those reviews. We may also share aggregated ratings and select excerpts from those reviews throughout our site.

Our human moderators verify that reviewers are real people and that reviews are authentic. They use leading tech to analyze text quality and to detect plagiarism and generative AI.

How GetApp ensures transparency

GetApp lists all providers across its website—not just those that pay us—so that users can make informed purchase decisions. GetApp is free for users. Software providers pay us for sponsored profiles to receive web traffic and sales opportunities. Sponsored profiles include a link-out icon that takes users to the provider’s website.

How To Build an ECommerce Business Plan

Whether you’re starting a new eCommerce business or moving your store online, a compelling business plan is foundational. Learn how to create one.

Due to the coronavirus pandemic, many small businesses have started including eCommerce in their business strategy. According to a recent survey, 34% of small businesses are now offering at least one product or service online. And some of them are reporting positive outcomes.

Take Texas-based Longhorn Meat Market for example. This century-old, family-owned business saw 152 new orders overnight and a significant increase in order volume after moving their operations online.

While there are definite perks to starting an eCommerce business, it involves considerable brainstorming and conceptualizing for logistics, marketing strategies, finances, etc. These details ensure that you don’t overlook any essential requisite. This is where an eCommerce business plan comes in.

From sourcing investment to making your first sale, this plan will play a key role at each step.

What is an eCommerce business plan?

An eCommerce business plan is the documentation of what your eCommerce business is or will be and how it will operate in the online space. It includes identifying the market you’ll tap into, the expected break-even point, the vision and mission of your business, and other such aspects.

Since sorting through all these details on your own might feel daunting, we’ve laid down some key steps to building an eCommerce business plan. Let’s take a look at these.

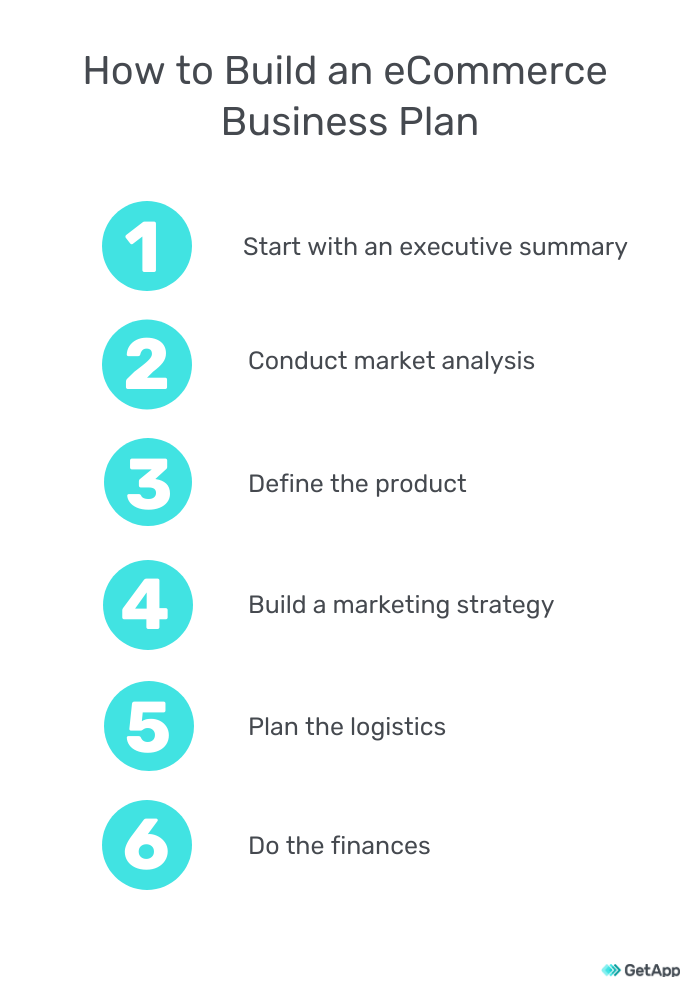

Step #1: Start with an executive summary

Before everything else, you need to lay down clearly what the business is (or will be) and where it is headed. If you’re already a functional eCommerce business, you could share an overview of the business concept, the team, current operations, and future goals. On the other hand, if you’re new to this game, you’ll need to elaborate on your vision, the founding team, and the business strategy.

This information is relevant to both investors and stakeholders. It will also help refine your own understanding of the business.

Here’s how you can create an executive summary:

Lay down the business details: Include information such as the business concept, vision and mission statements, and the business differentiator or unique selling point.

Include operational aspects: Capture a brief overview of the target market, the marketing and sales plan, current financial position (if you’re already generating revenue), projected profits, and the investment you’re seeking.

Introduce the team: Include an overview of the key members of the business. If the business is already functioning, this may include business partners and the C-suite executives. If you don’t have a functioning business, this may include the founding members.

FAQ: What should be the length of the executive summary in my business plan?

Answer: Since every business idea is unique, the length of the executive summary varies with the length of the overall business plan and the complexity of the business idea. However, executive summaries usually range between one and four pages as these can be printed into a one- or two-page brochure and shared with stakeholders.

Step #2: Conduct market analysis

This step will help you understand the industry and target audience. This analysis is foundational as it decides how your final product turns out. It consists of the following two steps:

Analyzing the industry: Identify the industry you’ll be operating in. For example, if your business involves selling packaged food items, then the target industry will be FMCG. Within this industry, if you cater to a specific market, such as low-calorie snacks, then this particular section will be your target market.

Identifying the target audience: Define the characteristics of the people who you want to eventually use your products/services. Considering the example of low-calorie snacks, your target audience will comprise health-conscious individuals with internet access and financially-equipped to spend a few extra dollars on low-calorie food.

Other factors that define your target audience may be geography, age range, gender, or profession.

FAQ: How do I calculate the size of my target market?

Answer: Although market size is not a must-have for a business plan, it’s certainly good-to-have as it plays a key role in defining the business strategy. The market size refers to the maximum revenue you can generate by selling a product.

Its calculation should be based on conservative estimates of the serviceable market you can reach given the competition in the market, your resources, sales channels, and product pricing.

Step #3: Define the product

Defining the product will help you clearly lay out its key characteristics, variations, and differentiating factors. A well-defined product will also help investors and stakeholders understand your core offering. Here’s how you can do this:

Identify the product categories: Create a broad overview of the categories your products fit into. In terms of the low-calorie snacks example, its product categories may include low-calorie protein bars, baked items, beverages, and crisps.

The key is to keep these categories broad so as to accommodate any sub-categories. For example, low-calorie baked items may branch into low-calorie cookies and tea cakes.

Define the product characteristics: Define other aspects of your product, such as their shelf-life, key differentiators, how you plan to source/create them, and where they will be stored.

FAQ: How can I differentiate my products from those of my competitors?

Answer: Some factors on which you can differentiate your products include: a unique feature (like gluten-free), product size (extra-large), manufacturing process (completely handmade), and ingredients (herbal or vegan). The design or branding of a product can also be a differentiating factor, such as the unique design of Crocs or the tailfins of a Cadillac.

Step #4: Build a marketing strategy

Once the market and the product are defined, you should draft a strategy to drive customers to your eCommerce space. For this, you’ll need to identify the right channels as they play a key role in increasing your chances of customer acquisition. The channels will vary depending on the type of product/service you’re selling.

You can include a mix of these channels in your marketing plan:

Organic: Organic marketing aims to bring in customers through search engine results, social media posts, and blogging websites. These channels don’t explicitly market your products or charge for the same but help build confidence as the audience knows you didn’t pay anyone to be in front of them.

To understand how to leverage these channels, ask yourself:

How can I make my social media posts more engaging?

What type of blogs might my audience find interesting?

How can I optimize my web pages to rank high in SERPs?

Paid: Paid marketing involves paying a certain amount to marketing channels for maximizing your exposure to the target audience. These channels include pay-per-click, pay-per-expression, pay-per-conversion, or similar marketing via Google Shopping, social media ads, affiliate marketing, influencer marketing, etc.

To understand how you may leverage this type of marketing, ask yourself:

Which social media channels does my target audience visit frequently?

Which affiliate marketing channels might be popular among my target audience?

Which social media influencers are aligned with the product/service I’m selling?

To manage various aspects of your marketing strategy, you can also consider using marketing software.

FAQ: How much should I spend on acquiring a customer?

Answer: To identify the cost of customer acquisition you need to first identify how much a customer might spend on your website throughout his/her lifetime. This could be slightly difficult in the early business stages as there won’t be much customer data to analyze. In this case, you may make a conservative assumption.

For example, if a customer is likely to spend $200 throughout his/her lifetime on ten low-calorie food items sold on your website, then subtract the cost of producing them, say $100, from this amount. The remaining $100 is the upper limit of what can be spent on customer acquisition. You can set an amount between $0-$100 based on your desired profit margin and marketing target.

Step #5: Plan the logistics

The logistics plan is essential for understanding how you will procure, ship, store, or manufacture products. This may not be as important while seeking investment as it is for your own understanding. To shape up this plan, look carefully at each leg of the logistics operations:

Production: Identify the suppliers from whom you’ll procure the raw material and the equipment you’ll use for manufacturing. Try to estimate how long the production and shipping period will be and how you plan to handle a sudden surge in demand.

Storage: Identify how much stock of raw material and finished products will need to be stored, and where. Also, plan to track all outgoing and incoming inventory.

Shipping: Determine if you’ll ship the products yourself or outsource shipping. These will, in turn, determine the additional staff you’ll need to hire or the resources such as packaging material you’ll need to procure.

FAQ: Should I manage shipping in-house or outsource it?

Answer: Both in-house and outsourced shipping have their own benefits and downsides. While in-house shipping provides greater control over the quality of service, outsourcing lowers upfront costs and promises expertise. While considering the in-house option, it’s essential to factor in reverse shipping as it involves substantial costs.

Step #6: Do the finances

Planning how to allocate finances is one of the most important parts of your business plan. Let’s see how you can do this.

Identify operating costs: Calculate the cost you’ll incur through various aspects such as rent of office space, warehouse rent, shipping costs, marketing budget, website hosting fee, and payment gateway transaction fee.

Make profit and loss projections: Find the difference between your projected expenses and revenue. Expenses will include every possible cost between the production and the sale of a product. Also factor in possible sales variations over time, promotions and offers, free shipping, and the fact that the whole inventory might not be sold.

Determine the break-even point: This is the point where your revenue equals all the expenses on setting up the business. In other words, your business turns profitable after this point. It’s particularly important for startups as most investors want to know how soon the company they are investing in will become profitable and yield returns.

FAQ: How do I identify the break-even point of my business?

Answer: To identify when you’ll reach the break-even point, divide the total fixed expenses (such as rent and IT) by the contribution margin, which is the difference between sales price per unit and variable costs (such as transaction fee and cost of raw materials).

Additional factors to consider

Creating a business plan for your eCommerce venture is not easy, but it’s certainly worth the effort. Here are some extra bits that will help you derive the maximum value out of your business plan:

Take notes: While creating the plan, you’ll identify several areas of ambiguity that will encourage you to think harder and get more clarity. These business areas may or may not make it into your business plan, but can come in handy after the business becomes operational.

Don’t dig too deep: Don’t expect all parts of your plan to convert into reality the way you envision them. Improvisation will be needed. For example, your sales may vary from the projections or certain seasons may turn out to be more profitable than others. So don’t add too much detail. A broad idea is sufficient!

Keep coming back: Your business plan doesn’t have to be a static piece of writing. You can (and should) keep coming back and making changes as your business grows. Constantly updating your business plan will ensure it remains fresh and relevant for the long haul.

Consider leveraging technology: Several areas of your eCommerce business can be automated using specialized software. These can help you manage financial reporting, marketing, shipping, and warehousing associated with your business. You can also opt for a software suite that helps manage your entire eCommerce operations from a single platform.

Bandita Awasthi

More on eCommerce

Sep 02, 2022

Aug 05, 2024

Jun 13, 2024

Sep 20, 2021